Several recent Inheritance Tax (IHT) announcements may significantly impact high net worth individuals (HNWIs) over the next few years. The extension of the current IHT threshold freeze to at least 2031, as well as imminent changes to the IHT treatment of unused pension funds and pension death benefits, means that now could be a good time to revisit your estate planning.

One way to mitigate a potentially large IHT bill is to insure your liability. You might have read Darren Berry’s take on this issue last year, ‘How to manage complex life insurance and estate planning as a HNWI’, which includes some important reminders and first steps.

Another valuable tool at your disposal is lifetime gifting. This can help to tax-efficiently lower the value of your estate by distributing assets while you are alive, rather than passing them on when you die. But robust record-keeping will be key to ensuring you and your loved ones avoid unwanted tax surprises.

Keep reading to find out more about the HMRC allowance you might use and why keeping track of your gifts is so important.

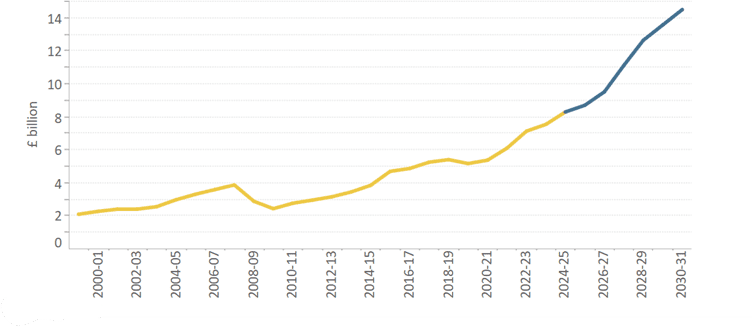

As Inheritance Tax receipts rise, the need for mitigation strategies increases too

The Treasury’s IHT receipts have been rising in recent years, in part due to frozen IHT thresholds. The nil-rate band has been frozen at £325,000 since 2009, while the residence nil-rate band (only introduced in 2017) has been frozen at £175,000 since 2021.

Latest forecasts from the Office for Budget Responsibility (OBR) suggest that IHT could raise £14.5 billion for the government by 2031.

Historic and projected IHT receipts (2000-2031):

Source: OBR

While frozen thresholds drag more estates into the IHT net, changes to the IHT treatment of pensions on death could have significant ramifications too. It’s possible that your pensions previously played a key role in your estate and legacy plans, but rule changes from 6 April 2027 may necessitate an adjustment.

Under current rules, benefits payable from a pension on death after the age of 75 are generally subject to Income Tax, payable by the beneficiary. New rules mean that unused pensions will also become part of the pension holder’s estate. This combination of IHT and Income Tax could result in a sharp rise in effective tax rates.

For this reason, planning to mitigate the effects of these changes could be a worthwhile strategy.

Gifting can be a tax-efficient estate planning tool

Lifetime gifting (or giving while living) can be a tax-efficient way to lower the value of your estate. Plus, it has the added benefit that you’ll still be around to see the difference your inheritance makes to those who receive it.

You can make as many gifts as you like during your lifetime, but once you have used up your HMRC gifting allowances and exemptions, the gifts you make will likely be classed as potentially exempt transfers (PETs).

These are subject to IHT at 40% on death within three years of making the gift, with tax charged on a sliding scale known as taper relief on death between three and seven years. Taper relief only applies if your total gifts made in the seven years before you die exceed the £325,000 nil-rate band.

Gifts that fall within HMRC gifting exemptions and allowances are IHT-free from the moment you make them.

It’s important to keep your records up to date, and yet Money Marketing suggests that 45% of HNWIs have no written record of the gifts they’ve made. While 29% rely on “mental notes”, 17% have no record at all.

Keep track of your £3,000 annual exemption to avoid unpleasant surprises

Each year, you have a £3,000 gifting allowance, known as the annual exemption. This is individual to you and can be carried forward for up to one year. This means that you and your partner could gift £12,000 this year if neither of you made use of your exemption during the last tax year.

Once gifts exceed £3,000, these could be subject to IHT if you pass away within seven years, so you could be inadvertently leaving your intended beneficiary with a surprise tax bill.

Gifts classed as “normal expenditure out of income” must pass strict HMRC tests

Record-keeping is arguably even more important if you plan to take advantage of the normal expenditure out of income exemption. This allows you to make regular gifts to loved ones, as long as your gift passes strict HMRC rules.

The gift must:

- Be made regularly and comprise part of your normal outgoings

- Come from your usual income (for example, a salary or pension)

- Not detrimentally impact your standard of living.

This exemption could be incredibly useful for paying into a child’s pension or a grandchild’s Junior ISA on their behalf, for example. But you’ll need to be able to prove to HMRC that each gift you make meets the above criteria.

Keep a simple record of the:

- Gift and recipient

- Value of the gift

- Date you gave the gift.

This should be sufficient to ensure these regular gifts don’t fall foul of HMRC rules.

Get in touch

If you want help revising your estate and legacy planning in light of imminent rule changes, get in touch with HFMC Wealth today. Contact us online or call 020 7400 4700 today to help plan your loved ones’ financial future.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.

The Financial Conduct Authority does not regulate estate planning or tax planning.