Half time chat.

As the whistle blows for half-time in 2026, we head back to the dressing room for a slice of orange and a short rest. It’s a chance to look back on a first half that started strongly, turned more challenging, but recovered somewhat by the end.

At the start of the year, we titled our outlook “A Year for Prudent Optimism”, expecting portfolios to make steady progress. That optimism was grounded in robust investment in US technology and increased military spending in Europe. Looking ahead to the second half, that view still feels broadly right, though now we’re putting more weight on the “prudent” than on the “optimism.”

To keep the sporting analogy going, this is not the time for overly expansive play. We’re not going fully on the defensive either, but we do think a more measured and disciplined approach is appropriate given the current backdrop.

The Waiting Game

Parents of a certain age with (largely) teenage daughters may well find themselves heading to Wembley shortly to watch one of the all-time greats*, Harry Styles. By the looks of the queues of happy youngsters singing their favourite Harry/Take That songs whilst streaming towards the Tube on the way home, patience remains a virtue.

*Editors Note: This is not necessarily the authors subjective opinion, but it has made my daughter happy. I am really looking forward to it.

For central bankers, patience will be the main dish in the months ahead. Whilst the re-opening of the Strait of Hormuz is clearly welcome, it is subject to potential setbacks. There will also be knock-on effects from the restrictions that have been in place for months now. Declining oil and gas prices will be swiftly felt and welcome, and the resumption (should it happen) of normal fuel supplies to Asia and Emerging Market economies will be particularly helpful given the consumer restrictions that have been in place.

There is, however, a growing risk that inflation drifts higher again, led in part by rising food prices as fertiliser supply remains constrained and costs increase. In the UK, the structure of the energy price cap also means households are likely to feel the effects of higher Gulf energy prices with a lag. Whilst we do not see this as the start of another sharp inflation spike, it does make it harder to see inflation returning to the elusive 2% target any time soon.

In our opinion, the good news is that while inflation is likely to rise in the near term, following a recent run of benign readings, it is less likely to increase to a level that would prompt the Bank of England to raise rates this year.

In the US, new Federal Reserve Chair Warsh has begun stamping his mark on the central bank. There was a much shorter statement at the June meeting. The statement largely was a statement of the obvious. This is in line with Chair’s desire for a reduced level of communication.

Before his confirmation, Warsh had made clear his dislike of the Fed’s large balance sheet and his preference for lower rates. Even so, the June meeting pointed more towards possible rate rises than cuts. For now, the Committee’s stated priority remains price stability.

The new Chair is a fan of the argument that the rolling out of AI within the economy will bring higher productivity. If so, this has a tendency to have a long-term downward pressure on prices. Whilst we have some sympathy with this opinion, this again is a waiting game. In the short-term, front and centre of focus should be the continued path for US inflation to be moving higher. Strong jobs numbers suggest the underlying health of the US economy is some way ahead of global peers, but not strong enough to be feeding any strong wage increases.

Over at the European Central Bank (ECB), the last thing policymakers wanted to do was to repeat the policy error of 2022. So, the last thing they did was to repeat a policy error. Raising interest rates, whilst pointing at more to follow, when inflation is only moderately rising and growth slowing, seems more about reclaiming authority, rather than steering the economy down a clear and certain path.

In Japan, the Bank of Japan continued its path of raising rates by another 0.25%, which contrary to the ECB, looks sensible considering a growing economy and firm inflationary pressures and positive wage growth.

So, in summary, we’re in a divergent world when it comes to central banks. The Bank of England will be sighing its relief at the most recent set of inflation numbers, that gives the green flag to hold rates still. The new Fed Chair might want to cut rates, but there is a time and place for everything, and this is neither. A rate hike is still possible, but that’s in the ‘wait and see’ pile. The Bank of Japan’s approach looks in step with its economy, whilst the ECB will be wishing they’d left it as it was.

Inflation: Sign of the Times

Whilst welcome, there should still be a degree of caution about the deal being brokered between the US and Iran. Until there is greater clarity on the final outcome, energy prices are likely to remain sensitive to the latest headlines. For now, however, the path away from hostilities, alongside a reopening of the Strait of Hormuz, has helped oil prices move lower.

On balance, our view remains that this period of elevated inflation is not a repeat of the surge seen in 2022–23, which was driven by several overlapping forces. This looks more like an energy-led headwind than a broad inflation shock, although the timeline remains hard to judge and will depend on how events unfold.

In the UK, the latest inflation reading remained at 2.8%, but it is expected to rise towards the mid-3% range through the year before drifting lower in 2027. Inflation is often discussed as a headline number. What matters more is how it affects households.

Rising prices are felt most keenly when they appear in regular, visible costs such as petrol, energy bills and groceries. These are prices people notice frequently, and they can quickly shape expectations about where prices are heading next. If households expect prices to keep rising, they may become more cautious about spending. That, in turn, can weaken consumer confidence and slow the wider economy.

The UK consumer is not in poor shape, but nor is there much sign of exuberance. Since the financial crisis, household debt has fallen steadily as a share of GDP, while aggregate savings remain above pre-pandemic norms. That provides some insulation against a renewed squeeze on household budgets. The problem is that savings are acting more as a buffer than a booster. After Brexit, the pandemic, the cost-of-living crisis, higher interest rates and the energy shock, consumer confidence has had plenty of reasons to stay subdued.

That leaves the UK consumer in saving rather than spending mode. With another rise in energy bills possible, real wage growth under pressure and labour market conditions softening, a consumer-led recovery still looks difficult to rely on. Unemployment is rising, vacancies are falling, and there is little evidence of the kind of labour market heat that would normally drive a fresh wage-price spiral.

The contrast with US households is striking. Rising prices and a long period of uncertainty have pushed UK and European households towards saving rather than spending. US consumers, by contrast, have been more willing to run down pandemic-era savings and maintain consumption. Larger tax refunds have also provided some support this year. That willingness to spend has helped underpin US growth, but it also leaves less margin for error if savings rates remain low and real disposable income growth weakens further. In short, the UK consumer has more of a savings cushion, while the US consumer has so far shown more willingness to spend.

To Infinity & Beyond?

The final half of the year is likely to see some high-profile private companies become public. To great fanfare Elon Musk’s rocket firm SpaceX listed on public markets in the United States in June, with an initial star-reaching $1.7tn valuation. Meanwhile, AI companies Open AI and Anthropic are also toying with the idea of a stock market debut with similarly high valuations. If press headlines can be interpreted, enthusiasm is running high. There is some justification given the future potential technologies that could transform and reshape entire industries in the years ahead. The real question is whether valuations reflect genuine potential, or just outright exuberance.

In the same way as enthusiasm builds to fever pitch every time England football teams reach a World Cup, there are reasons to stay measured to temper possible disappointment. A buoyant equity market can encourage private companies to seek elevated, perhaps even excessive valuations if and when they decide to list. With the rise of index-tracking funds (also known as passive investing), any new mega-cap stock joining a major index will inevitably be bought by passive investors regardless of the valuation. This dynamic not only magnifies initial market exuberance but should also raises a question too. If private companies can list at very high valuations, knowing passive funds will have to buy them, who decides whether public investors are getting a fair deal? With a valuation now eyeing the $2.2tn mark, for a business that is loss-making, that’s a question worth pondering.

That’s not to dismiss their genuine long-term promise; whilst the future technologies of these firms may indeed be revolutionary, a touch of caution remains wise for the investor. SpaceX is not profit making, has ‘challenging’ financial forecasts, and will remain under voting control of its founder. As we know from Toy Story, whilst Buzz Lightyear may well aim for the stars, even the most thrilling investment stories can come back to earth in time.

Growth and Inflation Numbers: Stagflating…

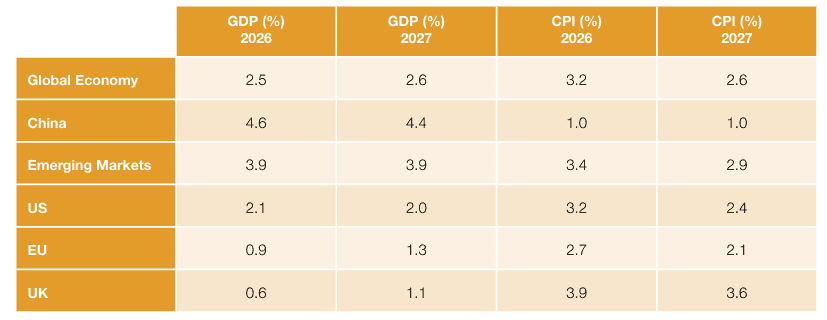

Thanks, as ever, to our friends at Schroders for the latest consensus forecasts, which are as of 6th May 2026 (note these were produced before the recent Iran war):

Source: Schroders Economic & Strategy Viewpoint, Q2 2026 (Data to 06.05.2026)

Since last quarter, there has been a trimming of the growth numbers for 2026, with the exception of emerging markets. Europe and UK consensus growth numbers fell more sharply, indicating the fallout from rising energy prices is weighing more heavily, given both are net importers of energy. Meanwhile, as an energy exporter, the US is more insulated than most. There’s not much to look forward to in the forecast either with consensus expectations for slower growth next year too.

A further point on inflation. That is the impact the huge amount of spending on Artificial Intelligence (AI) is having in the economy. This is helping to underpin a huge amount of business spending in the US economy and serves as another economic support. This is a positive, but it also brings inflationary pressures from the increased demand for components and strong demand for energy from data centres.

Overall, the picture is one of slow and weakening growth, while inflation remains higher than central banks would like. Energy is still the main pressure point.

Equity Markets – Going Up and Down at the Same Time.

If you ignored the news headlines and looked only at the level of stock market indices, you might conclude that all was well with the world. So, with so many challenging headlines, how have equity markets kept rising?

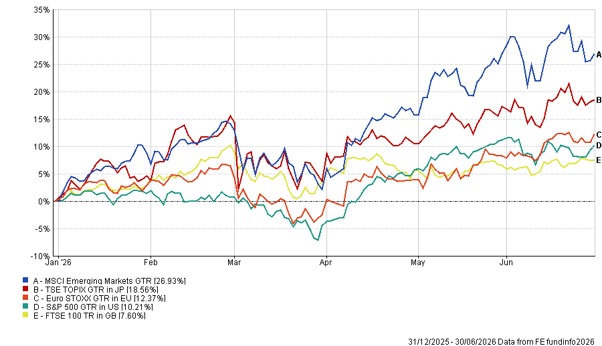

The second quarter saw equity markets recover from the weakness that followed the escalation in Middle East tensions, helping to lift the broader market mood. AI-related shares also moved higher, particularly semiconductor manufacturers, where earnings growth has been exceptionally strong. Encouragingly, that improvement has started to broaden beyond a narrow group of technology winners, both across different parts of the technology sector and across regions.

The chart below shows year-to-date performance across several major indices (all in local currency). Emerging markets are leading the way, helped by their meaningful exposure to technology, particularly Taiwanese and South Korean semiconductor companies.

Energy shares have also performed strongly. In the near term, they have been supported by supply disruption around the Strait of Hormuz. Longer term, the sector may also benefit from the structural energy demand created by AI, particularly through the rapid growth of data centres.

There has been some talk of market bubbles, but the valuation picture is more mixed than that. Strong earnings growth from AI-related technology companies and energy stocks has helped bring headline valuations down since January. Even so, cycles still matter. They show up in valuations, earnings and investor behaviour, and we are clearly in the middle of a powerful new technology cycle.

At this early stage, companies are spending huge sums to build the infrastructure needed for AI. So far, markets have rewarded that spending with strong share price gains and impressive earnings growth. The recent strength in semiconductor earnings is unlikely to continue at the same pace forever, but the wider AI theme still has momentum. Risks remain should earnings start to slow, or if investors stop rewarding large capital spending plans with higher share prices.

We continue to hold meaningful equity risk at a level that is appropriate for each risk profile. We also continue to maintain diversified portfolios, shying away from areas with the highest valuations and holding broadly diversified portfolios. We continue to diversify portfolios across regions, sectors and styles, so that outcomes are not driven by a single, dominant force.

Fixed Income – Bond is Back

I was reading about the search for a new James Bond recently and whether the new 007 should be more, well, let’s just say a bit more relevant for the current day and age.

For the period after the financial crisis up to 2022, bond markets found themselves in a similar crisis of confidence. With central banks driving bond yields ever lower, fixed income funds had to work increasingly hard just to avoid losing money, let alone making it. But with yields reset after 2022’s interest rate rises, bonds are very much back. So, what should you expect from a fixed income fund?

Fixed income should provide capital preservation, a return ahead of inflation, low volatility and an income stream. These are the steady plodders doing the heavy lifting. Equities are the glory seekers who typically provide higher returns over the long term but with far higher volatility.

If fixed income can deliver a mid-single digit return without causing too many sleepless nights, it is doing the job investors need it to do. This is especially important for lower-risk investors, who usually hold more in bonds and therefore rely more heavily on them to meet their long-term objectives. Today, fixed income is broadly playing that role again, although it is worth remembering that bond markets can still have difficult years. 2022 was a clear reminder of that.

There is still uncertainty over the near-term path of interest rates and inflation, but we remain focused on the longer-term opportunity. In fixed income, the starting yield matters a great deal to future returns. Put simply, buying good-quality bonds when yields are more attractive tends to improve long-term return prospects.

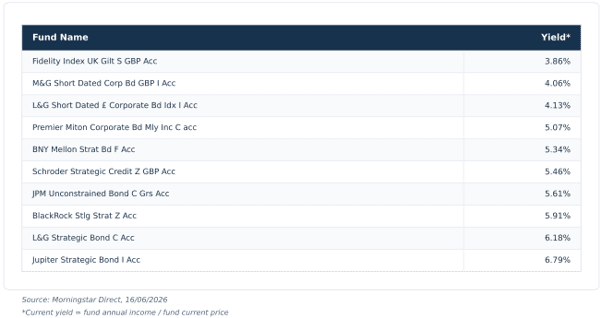

When we talk about yields, current examples on funds that are across some of our portfolios are:

That does not mean the next few months will be straightforward. Interest-rate volatility may remain elevated, and inflation risks have not disappeared. In portfolios, we have therefore focused on capturing the income available from bonds while limiting exposure to larger price swings that can be driven by movements in interest-rate expectations. In practice, that means a greater emphasis on shorter-dated, higher-quality areas of the market, alongside a selective approach to credit risk.

Fixed income returns come from three main sources: the income paid by the bond, changes in interest rates, and shifts in credit risk. We remain positive on the first, more cautious on the second, and selective on the third. The aim is to keep the bond portion of portfolios working as it should: providing attractive income, supporting diversification and helping act as a shock absorber if markets become more unsettled.

Conclusion: You Can’t Win a Match at half-time.

As we head into the second half, the investment backdrop feels neither especially gloomy nor especially forgiving. Inflation remains an irritant and economic growth is hardly racing away. Central banks would like to cut rates if they can, which would be a support, but need to keep their eye on inflation for now.

Equity markets have continued to make progress, helped by strong earnings in the technology sector and renewed excitement around AI. There are good reasons for that enthusiasm, but valuations still leave less room for disappointment in some of the most popular areas. We are therefore happy to keep meaningful equity exposure where it is appropriate for each portfolio, but continue to prefer balance over bravado. Diversification across regions, sectors and investment styles remains important, particularly with markets increasingly concentrated.

Fixed income is also doing a more useful job than it did for much of the post-financial-crisis period. Higher starting yields mean bonds once again have the potential to provide income, diversification and a degree of ballast if needed. That does not mean every part of the bond market is equally attractive, or that the path will be smooth. We remain focused on good-quality areas, shorter-dated opportunities and a selective approach to credit risk.

Overall, our message is a familiar one: stay invested, stay diversified and avoid being pulled too far in either direction by the crowd.

In this world-cup year, this is about ‘controlling the controllables’, not for showboating near your own penalty area. All teams need ‘top, top’ players, but the strength of the team overall is the most important.

Our portfolio strategy is unchanged. We aim to capture the income available from bonds, hold equities to benefit from long-term growth, and maintain enough discipline to avoid chasing every passing theme.

As ever, on behalf of the entire investment team, Amaraj, Becky, Hayley, Kim, Will and myself, thank you for the trust you place in us to manage your portfolio.