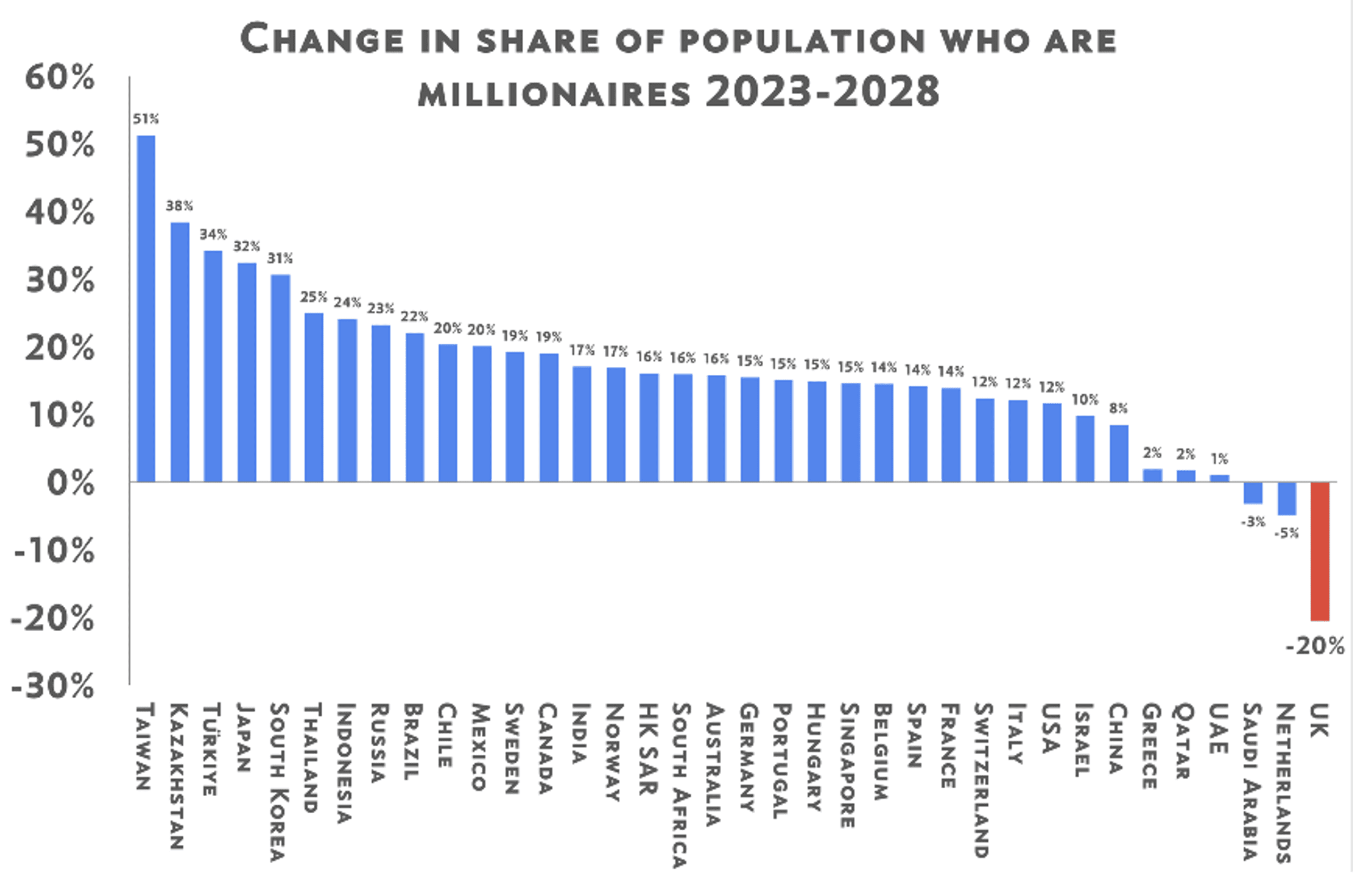

Pre-budget analysis from the Adam Smith Institute predicts that the share of the UK population who are millionaires may fall by as much as 20% by 2028.

This forecast decrease, from 4.5% of British residents to just 3.6%, would represent the biggest fall of any other major developed country over the same period. And it could have a significantly detrimental effect on the UK economy.

Why might this potential “millionaire exodus” take place? How might the Autumn Budget have exacerbated the problem? And why might professional tax advice mean that someone contemplating a move abroad may not need to act just yet?

Keep reading to find out.

Millionaires play a vital role in the UK economy but an increasingly challenging tax environment is encouraging more to leave

A loss of up to 20% of Britain’s millionaires by 2028 would be proportionally more than any other major economy in the world and unhelpful to the prospects for growth of the UK economy over this time frame.

The figures suggest that only the Netherlands and Saudi Arabia are also set to lose millionaires between 2023 and 2028, with forecast drops of 3% and 5%, respectively.

This potential loss of UK millionaires is worrying and potentially upsetting for the individuals concerned, but there are wider implications too. Millionaires often represent a large portion of a nation’s wealth creators.

They might be business owners, for example, who are responsible for employing large numbers of staff. They also tend to contribute significantly to the Treasury’s annual tax take, money that is crucial for helping to fund public services.

The top 1% of earners, for example, pay 29.1% of Income Tax (according to the Institute for Fiscal Studies), the Treasury’s largest source of tax revenue.

This research was released before the Autumn Budget, which, when it came, did little to dispel concerns for many high net worth individuals (HNWIs) and their families.

Financial advice can help to mitigate tax increases and keep your plans on track

Professional financial advice can help you to build long-term plans, aligned to your goals and personal circumstances. These plans, while clearly affected by external events like government and legislative changes, can also be robust and adaptable.

With careful planning, someone contemplating leaving the UK may find that such drastic action is unnecessary. In the current climate, skilled and relevant advice is more important than ever.

Advice can help in many key areas of your finances throughout this parliament and beyond. Here are just three.

1. CGT rates increased

Rachel Reeves used her Autumn Budget to announce a rise to Capital Gains Tax (CGT) rates, effective from 30 October 2024.

The basic rate of CGT increased from 10% to 18% and the higher rate from 20% to 24%. Thankfully, for those affected, this still leaves the UK with the lowest rates of CGT throughout the G7, albeit higher than before.

If you’re looking to dispose of high-value assets in the near future, speaking to your adviser can help. There may be actions you can take to minimise the impact of these changes.

2. Be careful how you withdraw your “retirement super pot”

A recent Freedom of Information request, reported by the Independent, has uncovered that the 25 biggest annual incomes from UK pensions in 2023/24 were around £2,982,000. A further 8,000 retirees received £100,000 or more during the tax year.

There are significant tax implications of taking such large sums. Be sure to think carefully about the size – and the timing – of the withdrawals you make.

Budget changes to Inheritance Tax rules for unused pension pots mean that from 2027 you might need to think differently about how pensions fit into your estate planning. These measures are still subject to consultation but change is likely.

For now, be sure to make full use of the tax efficiencies your pension and other products offer and consider the other tax-efficient actions you might take. Your adviser will be able to discuss the many avenues potentially open to you in this regard.

3. Non-domiciled (non-dom) status rule changes are in the offing

As predicted, the chancellor chose to abolish the non-dom tax regime, although not – as was the case with the CGT rate changes – effective immediately.

The regime will exist in its current form until April 2025, when it will be replaced by a residence-based scheme, which, it is said, will provide incentives to investors and wealthy foreigners to come to the UK temporarily. Whether this will prove tempting or not remains to be seen.

What is clear, though, is that this measure has the potential to tip many HNWIs into leaving the country, with some high-profile casualties already going public. That does not mean, however, that this is the right action for all.

If you are worried about the implications of recent tax changes, please get in touch about possible next steps.

Get in touch

To find out how expert tax advice can help you manage an increasingly challenging environment for high earners and HNWIs, please get in touch.

Contact us online or call 020 7400 4700.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance. The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.