A Narrower Path

We began this year with an Investment Strategy titled “A Year for Prudent Optimism”. At the time, our view was that portfolios could continue to make steady progress. Significant amounts of investment in areas such as technology remained supportive, particularly in the US, whilst in Europe, greater investment in military expenditure served as an economic support too.

There was also a growing expectation that central banks, particularly here in the UK, would start cutting interest rates. That said, we also recognised that rising markets in 2025 had made some parts of the equity market become more expensive, which was making it a narrower path to navigate.

The first couple of months seemed to support this view. Markets performed well through January and February, building the momentum of last year. Conditions became more challenging during March as geopolitical tensions escalated following the conflict involving the US, Israel and Iran. This resulting disruption in oil and gas supplies through the Strait of Hormuz, increased uncertainty and market volatility. By the end of the quarter, the gains made during the first two months had been wiped out.

In periods like this, it is important to balance conviction with healthy doses of flexibility. While we base our investment decisions on a clear central view of how events are likely to unfold, fast‑moving markets can quickly challenge assumptions. Rather than reacting to short‑term noise, our approach allows portfolios to adapt as conditions change, helping to manage risk while remaining positioned for longer‑term opportunities. It is also worth remembering that this is a very real crisis for the people of Iran and wider region, who face a deeply uncertain and difficult future with profound human consequences

Energy Matters

The events in the Strait of Hormuz have caused significant disruption to supply and rising prices as a result. The immediate implication of the disruption is straightforward, in that the longer it lasts and the greater the damage to oil infrastructure:

- Longer disruption → longer recovery

- Longer recovery → higher energy costs for longer

- Higher energy costs → more inflation pressure

- More inflation pressure → potential drag on growth

Today, markets would settle for a lower-intensity, contained conflict – one which allows for the re-opening of oil supplies over the next month or two, with hostilities fading into occasional flare-ups, rather than continuous engagement. Whilst this outcome may suit the US, it is unlikely to be welcomed in Tehran given the significant economic damage Iran can still inflict at relatively little cost. This remains one of its most effective sources of leverage in a war in which it is not a military equal for deterring further action, both now and in the future.

The risk of escalation cannot be discounted. Persian Gulf countries, which initially opposed the war, are now suffering falling energy revenues with limited exports and damage to energy infrastructure. If Iran continues its attacks on their facilities, they may feel compelled to join the military intervention, potentially broadening the conflict.

Further targeted attacks on any energy infrastructure run the risk of a sharp deterioration for markets under the weight of more energy price rises.

There are real risks ahead, and we do not want to underplay them. However, the most extreme outcomes are typically the least likely, even during periods of severe stress such as COVID or the Russia/Ukraine shock in 2022, when companies and households proved able to adapt through the most challenging phases. For portfolios, this means we need to remain vigilant and be prepared to adapt as events unfold.

Interest Rates and Inflation

In short, the energy shock complicates the inflation outlook and may delay rate cuts, but it does not, in our view, fundamentally alter the medium‑term direction of lower interest rates.

Having trimmed this section back in recent quarters, interest rates and inflation have moved to the forefront again and warrant renewed attention. The reason is straightforward: energy prices have risen sharply following the war in Iran and subsequent disruption to shipping through the Strait of Hormuz. Higher energy costs tend to feed into household bills and business costs, which can push inflation higher in the near term.

As a result, expectations for interest rate cuts have been pushed further back. However, there are good reasons to avoid thinking this a re-run of the inflation spike of 2022. Markets can move quickly on headlines, and in March there were moments when market pricing briefly flirted with the idea that UK rates might rise significantly. That did not look plausible to us at the time and has since been partially reversed. The UK economy was already in the slow lane, and there are no strong reasons for thinking we are about to move into a higher‑growth environment. If rate cuts are postponed for long, it becomes harder for demand to pick up. Elevated borrowing costs would continue to burden households and businesses, especially with energy bills also climbing.

Since the onset of the crisis, we initially thought central banks would look through short‑term energy price pressures, focusing instead on weak growth and rising unemployment. This still may happen. Today, rate rises remain far from certain (particularly in the UK), but the momentum towards lower interest rates has clearly been interrupted. The Bank of England adopted a more hawkish tone, cautioning that higher energy and commodity prices will raise near‑term inflation and that it is alert to the risk of more persistent domestic inflation if second‑round effects take hold.

The near‑term risk is that official interest rates either remain higher for longer, or even rise modestly, before ultimately having to fall more sharply as the already fragile economic conditions come under pressure from weaker demand, higher financing costs and rising unemployment.

On inflation, there are several reasons why we do not think this is a repeat of the last energy price shock of 2022/23. Then, the rise in UK inflation arrived in three overlapping waves. First came goods inflation, driven by supply constraints as economies emerged from COVID‑19 lockdowns and demand for goods surged. Then, before goods inflation had peaked, a second wave hit as the war in Ukraine pushed energy and food costs higher. Finally, as economies continued to re‑open, labour found itself in a position of strong bargaining power, with more vacancies than people to fill them. That helped drive stronger wage momentum and stickier services inflation.

The chief point is that the inflation spike of 2022 had multiple, cumulative causes, not a single driver.

That matters because it helps frame today’s question: are we facing a single‑wave shock, or something that spreads into wider knock‑on effects?

Energy prices have clearly risen quickly. At the end of March, Brent Crude was around $109/barrel, having been around $60 in January. That is consistent with the early stages of a new energy price shock. The key question is whether it remains concentrated in energy, or whether it broadens into second‑round effects — for example, higher wage demands and more widespread price rises. With inflation dropping back and job vacancies falling strongly in recent years, we struggle to see a strong starting point for rising wages.

While higher energy prices are a global issue, Asia faces an additional complication: the effective closure of the Strait of Hormuz has turned what could have been “just” a price shock into a supply disruption risk. Because a very large share of Gulf energy flows ultimately ends up in Asia, a prolonged interruption has the potential to be felt more sharply there—both through higher prices and through availability. That is a risk worth keeping a close eye on, not least because it can spill over into global trade and confidence.

Whilst the focus has been on rising energy prices, supply disruptions are also happening to fertilisers, which has consequences for rising food prices, sulphur which feeds into industrial processes could lead to bottlenecks, and commercial helium which is also used in healthcare and in the technology sector for chip manufacturing.

That brings us to inflation expectations, which matter almost as much as the inflation data itself. For many of us, petrol and grocery bills are the most visible signs of inflation and they shape how confident we are about spending. You might buy a new phone every few years, but you notice bread, milk and fuel every week and it’s those frequent price signals that can change consumer behaviour. With consumption making up the bulk of economic activity (particularly in the US, and meaningfully so in the UK), anything that dents willingness to spend quickly feeds back into weaker growth prospects.

Overall, the current energy shock complicates the inflation outlook for central banks. It at least delays interest rate cuts and increases the prospect that rates stay higher for longer in the near term. On balance, our view is that this is not a repeat of the inflation surge seen in 2022–23, which was driven by multiple overlapping factors. But it is a headwind for now, with a timeline that remains hard to judge. As events unfold our view may need to evolve too.

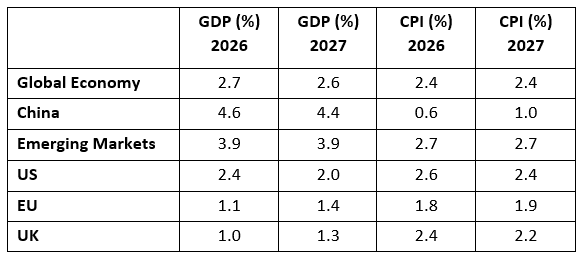

Growth and Inflation Numbers: Under Pressure

Thanks, as ever, to our friends at Schroders for the latest consensus forecasts, which are as of 3rd February 2026 (note these were produced before the recent Iran war):

Source: Schroders Economic & Strategy Viewpoint, Q4 2025 (Data to 03.02.2026)

The broad message is familiar: modest growth, with inflation not quite disappearing. Inflation pressure points are around energy, and that matters because energy costs don’t just nudge headline inflation they hit household confidence and spending decisions quickly.

In the United States, fiscal support is coming through in the form of larger tax refunds linked to last year’s One Big Beautiful Bill Act. A few weeks ago, that looked like a straightforward tailwind for consumer spending, it now looks more like a buffer as affordability concerns mean some households may now use that cash to absorb higher petrol and utility costs rather than to step up discretionary spending.

The same “buffer not booster” logic arguably applies in the UK, where consumers have been reluctant to loosen the purse strings for some time. With another rise in energy bills on the horizon, it would be no surprise if households stay cautious a little longer and for growth forecasts to be downgraded. The UK consumer remains in a saving, not spending, mode. That saving habit does provide some insulation against an energy squeeze, but it also highlights how households are behaving defensively. With real wages drifting lower and expected to come under further pressure if inflation stays elevated, a consumer-led recovery still doesn’t look to be on the cards. Unemployment is rising and job vacancies are falling. There is no clamour from employers seeking staff, or from workers looking to move to higher-paid positions.

Portfolio Outlook

Equity Markets – Moving forward, but with some more caution in the near term.

As noted earlier, equity markets entered the year with a fair degree of optimism. Inflation has fallen from its peaks, expectations were for interest rates to be heading lower, and corporate balance sheets are generally in reasonable health. We still believe that over the long term, these remain supportive conditions for investing in shares, but the near‑term backdrop has become more complicated. The war in Iran has introduced a fresh headwind for markets in the near term. Geopolitical shocks often feed into markets through familiar routes: energy prices, inflation expectations, and confidence. If the oil price remains elevated, inflation will prove stickier and complicate the outlook for interest rates. And when uncertainty rises, markets can become more risk averse, even if the long‑term fundamentals haven’t materially changed.

It is also worth remembering during 2025 was a strong year for equity markets, with valuations broadly rising. This has reduced the amount of cushion available for investors and therefore left less room for disappointment. That doesn’t mean a downturn is inevitable, but it does mean we are walking along a narrower path than we may have been used to.

Over quarter end we trimmed some equity risk in portfolios where we felt it was necessary given the strengthening case for having a slightly more cautious stance in the near term. In other words, we took a little bit of risk off the table.

Importantly, we continue to hold meaningful equity risk at a level that is appropriate for each risk profile. This was an adjustment at the margins, rather than a wholesale change. We also continue to maintain diversified portfolios, shying away from areas with the highest valuations and spreading exposure across regions, sectors and styles to prevent portfolio outcomes being driven by binary forces. The exact changes made do vary by portfolio range and risk profile.

Fixed Income – still attractive income, but less certainty over the pace of rate cuts.

In fixed income markets, the key challenge remains uncertainty around the path of interest rates and inflation. While inflation has eased a long way from the highs of 2022, it is still too early to be confident that it will settle quickly and smoothly at central bank targets. The war in Iran and rising price of energy only makes central banks jobs more challenging.

Today, the headline levels of yield that fixed income offers remain attractive, so it is important to take advantage of it, whilst managing interest rate risk. In portfolios, the focus has been on capturing the income potential of bonds, while reducing exposure to big price swings driven by interest rate volatility. In practice, that means investing more towards shorter‑dated, higher‑quality parts of the bond market, and taking a more careful approach to credit risk. Hence, we made further adjustments in fixed income allocations where appropriate, to reduce the overall portfolio sensitivity to interest rates and increase the focus on quality.

Fixed income returns ultimately come from three places: the yield, movements in interest rates, and changes in credit risk. Whilst we are still positive on the first, we are more cautious on the second and continue to be selective on the third. The aim is to keep portfolios well‑balanced and to capture the attractive income that is available, whilst continuing to make the fixed income portion of portfolios perform the traditional defensive role it should, even if the next few months prove a little noisy. In other words, we want your bonds not just to pay you a decent income, but also to serve as a safety net if markets get turbulent.

Conclusion: Continuing to navigate a narrower path.

Rising valuations over 2025 in equity markets made for a narrower investment path for investors to navigate. The war in Iran is a noteworthy hurdle that complicates matters further and is an unexpected setback to the view that markets can still make headway.

In portfolios, we have focused on continuing to build diversified positions and have tended to shy away from areas where valuations looked most expensive. This may have been a headwind at times, but we maintain that in an environment such as this, receiving a series of regular cashflows into portfolios is a helpful underpin to long-term returns, whether it is from fixed income holdings or equity funds that deliver dividends.

Please remember that markets do get disrupted, more often than we tend to remember after the passing of time. More importantly, over the long-term, markets do tend to move forward. We do not expect that trend to be disrupted despite the headlines today, but we do think the near-term could be more problematic, so have made some small adjustments to both fixed income and equity holdings where appropriate.

As ever, on behalf of the entire investment team, Amaraj, Becky, Hayley, Kim, Will and myself, we thank you for the trust you place in us to manage your portfolio.